21 Smart Life Insurance Renewal Tips 2025 for Better Coverage & Savings

Published on August 5, 2025

Emma Carter

Senior Insurance Editor

Emma Carter is a senior insurance editor with 12 years in P&C publishing and agency work; she simplifies policy details for everyday readers.

Understanding Life Insurance Renewals in 2025

Renewing your life insurance policy might seem like a routine task, but in 2025, it’s more important than ever to approach it with strategy and awareness. With recent shifts in the economy, regulatory changes, and technological advancements, what worked in 2020 might not cut it now.

What Is a Life Insurance Renewal?

Life insurance renewal refers to continuing your existing policy after its term expires or making updates to maintain your coverage. Term life policies often require active renewal at the end of a specified term, while permanent life policies may simply require payment of ongoing premiums.

During a renewal, you can:

- Reassess coverage needs.

- Modify policy details.

- Update beneficiaries.

- Add or remove riders.

- Adjust premium payments.

Why Renewing in 2025 Is Different

In 2025, digital tools and evolving regulations have made renewals more dynamic. Insurers now offer AI-driven comparisons, automatic risk assessments, and mobile-first platforms. That means smarter policy management—but also more complexity if you're not prepared.

Some key differences in 2025 include:

- AI underwriting models adjusting your premium in real time.

- Hybrid policies combining life and health coverage.

- Stricter compliance for policy disclosures and beneficiary designations.

Major Changes to Expect in Life Insurance Policies in 2025

Understanding what's new can help you make more informed decisions during your renewal process.

Regulatory Updates

New global and national regulations demand more transparency in how insurers calculate premiums and assess risks. In the U.S. and Europe, regulators now require clearer disclosures of policy terms, rider costs, and exclusions.

Market Trends Impacting Renewals

Key trends include:

- More competitive pricing due to digital-only insurance startups.

- Emphasis on wellness-based incentives (like discounts for healthy habits).

- Greater demand for eco-conscious and ethical investing-linked policies.

Digital-First Insurance Platforms

Online policy management is no longer optional. In 2025:

- Most providers offer digital dashboards.

- You can set renewal alerts via mobile apps.

- AI bots help you compare and renew in minutes.

Tip #1–3: Review Your Coverage Needs

As life evolves, so do your insurance needs.

Assess Life Events (Marriage, Kids, etc.)

Got married, had a child, or bought a home in the last year? Your coverage should reflect those responsibilities.

Check Financial Goals Alignment

Ensure your policy matches your current financial goals. Are you saving for a child’s college or aiming for early retirement? Your policy should support that vision.

Understand Term vs. Whole Coverage

Reconsider your insurance type:

- Term: Cheaper, short-term protection.

- Whole/Universal: More expensive but builds cash value.

Tip #4–6: Evaluate Your Premiums

Let’s not overpay.

Compare New Premium Rates for 2025

Use online tools to shop around and see if you’re getting the best deal based on your age, health, and risk factors.

Consider Health-Based Discounts

Some insurers offer better rates if you’ve improved your health or maintained a healthy lifestyle—like quitting smoking or reaching a healthy BMI.

Watch for Inflation Protection Add-ons

Premiums might stay fixed, but real-life expenses don’t. Consider adding riders that account for inflation to protect your future payout value.

Tip #7–9: Beneficiary Updates

One of the most overlooked yet critical parts of a life insurance renewal is making sure your beneficiary details are accurate and up-to-date.

Add or Remove Beneficiaries

Over time, your family dynamics may change. You may need to:

- Add a new spouse or child.

- Remove an ex-spouse after a divorce.

- Include a legal guardian or trustee for minor beneficiaries.

It’s essential to formally update these in your policy. Verbal instructions or a will do not override the beneficiary listed in your insurance contract.

Avoid Legal Disputes

Outdated or vague beneficiary information can lead to disputes, delays, and even lawsuits after death. Prevent this by:

- Naming full legal names.

- Specifying the relationship.

- Allocating exact percentages.

Keep Beneficiary Contact Details Current

Make sure your insurer has correct addresses, phone numbers, and identification for your beneficiaries. This speeds up the claims process and avoids unnecessary stress for your loved ones.

Tip #10–12: Review Riders and Add-ons

Riders are optional features that enhance your policy. At renewal time, you should re-evaluate them based on your current lifestyle.

Evaluate Critical Illness Riders

This rider provides a lump sum payout if you’re diagnosed with certain illnesses like cancer or stroke. In 2025, more insurers are expanding the list of covered conditions.

Consider Waiver of Premium Benefits

This rider waives future premium payments if you become disabled and can’t work. It’s a powerful tool for income protection and peace of mind.

Add Accidental Death Coverage

Accidental death benefits increase the payout if you die in a covered accident. These riders are especially useful for:

- Frequent travelers.

- High-risk occupations.

- Active lifestyles.

Tip #13–15: Policy Portability and Conversion Options

If you're moving jobs or switching from group to personal coverage, these tips are for you.

Convert Term to Permanent Insurance

If your term policy is ending, consider converting it into a permanent policy without needing to requalify medically. This is a great option if your health has changed.

Explore Employer-to-Private Portability

Leaving your job? Some group insurance policies allow you to port coverage to a personal plan. This ensures you’re never without protection.

Avoid Lapsed Policies

Always set up:

- Auto-payments.

- Email/SMS reminders.

- Policy alerts through your insurer’s app.

A lapsed policy can cost you more in the long run—especially if your health status has changed.

Tip #16–18: Use Technology to Your Advantage

2025 is the era of digital insurance. Use tech to make your renewal seamless.

Set Digital Renewal Reminders

Most insurers offer digital portals where you can:

- Set up automatic reminders.

- Review documents.

- Update information quickly.

Compare Policies with AI Tools

AI-powered comparison platforms can analyze dozens of policies in seconds, giving you personalized suggestions based on:

- Age.

- Health.

- Budget.

- Goals.

Manage Policies via Mobile Apps

The best insurers now provide robust apps to:

- Track policy performance.

- Upload documents.

- Schedule virtual meetings with advisors.

Tip #19–21: Work with an Insurance Advisor

A licensed professional can help you navigate the complexities of policy renewal.

Schedule Annual Policy Reviews

Each year, meet with your advisor to:

- Evaluate changes in your life.

- Assess your financial goals.

- Optimize your policy performance.

Discuss Future Financial Planning

A good advisor will look beyond just insurance. They’ll:

- Help integrate your policy into your estate plan.

- Offer investment guidance if you have a cash-value policy.

- Identify tax-saving opportunities.

Understand Legal and Tax Implications

Some policies can:

- Affect estate taxes.

- Trigger capital gains.

- Influence Medicaid eligibility.

Make sure you’re not caught off guard.

Mistakes to Avoid During Life Insurance Renewal in 2025

Mistakes can cost you money—or worse, leave your family unprotected.

Ignoring Policy Lapses

Missing a premium deadline—even by a day—can trigger a lapse. Always set up auto-payment options and back-up payment methods.

Not Disclosing Health Changes

If your insurer requires a new medical review, be honest. Hiding health issues can void claims later on.

Automatically Renewing Without Review

Renewing “as is” without a review means:

- You may be overpaying.

- Your coverage might be insufficient.

- Beneficiaries may be outdated.

How to Maximize Value from Your Renewed Policy

Get more out of your coverage with these smart strategies.

Bundle with Other Insurance Products

Many companies offer multi-policy discounts if you bundle life, auto, or home insurance.

Claim Free Loyalty Bonuses

Some insurers provide loyalty rewards like:

- Cashback.

- Premium discounts.

- Increased coverage after a no-claim period.

Use Cash Value Efficiently

If your policy has cash value:

- Borrow against it for emergencies.

- Let it grow tax-deferred.

- Use it to pay future premiums.

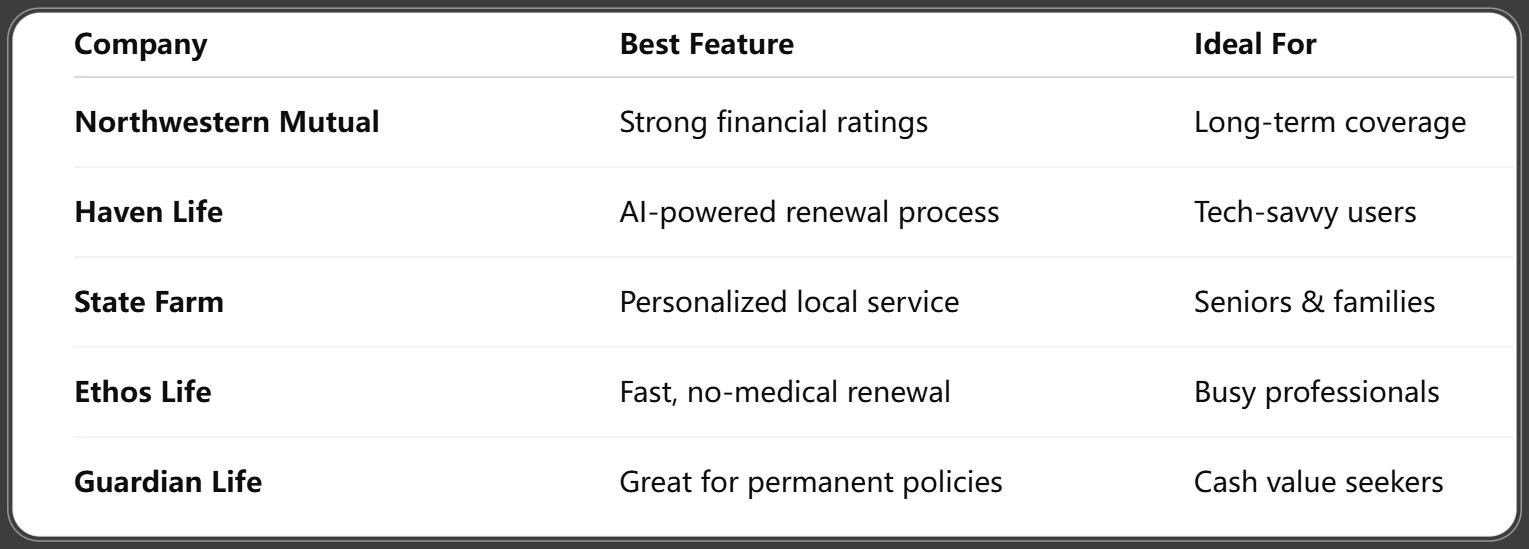

Best Life Insurance Companies for Renewals in 2025

When choosing a provider, consider their renewal terms, support, and tech.

MoneyGeek. (2025, May 30). Life Insurance Facts, Stats and Coverage Trends. Retrieved May 30, 2025.

Checklist Before Renewing Your Policy in 2025

Use this 10-point checklist to stay on track:

- ✅ Review your current policy.

- ✅ Update personal information.

- ✅ Confirm or change beneficiaries.

- ✅ Assess life changes (marriage, children, job).

- ✅ Compare premiums and quotes.

- ✅ Review or add riders.

- ✅ Set up auto-payment.

- ✅ Consult a financial advisor.

- ✅ Read the renewal terms.

- ✅ Confirm receipt of updated policy.

Expert Insights on Life Insurance Trends in 2025

Top financial advisors predict:

- More hybrid products combining health, life, and savings.

- Increased use of biometric tracking for dynamic premium pricing.

- Greater demand for sustainable investment-linked policies.

"In 2025, policyholders who take time to review and understand their renewals are the ones who’ll get the most value." – Maria Thompson, CFP®

FAQs About Life Insurance Renewal Tips 2025

1. Can I renew a lapsed life insurance policy?

Yes, but you may need to undergo a medical exam or pay a reinstatement fee depending on how long it’s been lapsed.

2. Does my premium increase at renewal?

It can—especially for term policies. But shopping around or switching insurers can help keep costs down.

3. What’s the best time to renew my policy?

Start the process at least 30-60 days before the expiration to avoid coverage gaps.

4. Can I change my coverage amount during renewal?

Absolutely. You can increase or decrease your sum assured based on your current needs and financial goals.

5. Do I need to tell my insurer about health changes?

If your policy requires a new medical review, yes. Always be honest to avoid future claim denials.

6. Is it better to convert my term policy or buy a new one?

It depends on your age, health, and financial situation. Converting helps avoid new medical exams, but new policies may offer better rates or features.

Conclusion: Renew Smart, Stay Protected

Renewing your life insurance policy in 2025 doesn’t have to be a hassle. With a proactive approach, digital tools, and expert guidance, you can turn it into an opportunity to upgrade your protection and reduce your costs.

Don’t treat it as a routine task—see it as a vital part of your annual financial check-up. And remember, the best time to review your life insurance is before you need it.

You Might Also Like

Life Insurance Medical Exam 2025: 20 Insider Tips for Faster Approval & Better Rates

Aug 5, 2025Guaranteed Issue Life Insurance 2025: 18 Essential Facts You Must Know

Aug 5, 2025Life Insurance for Millennials 2025: 19 Smart Moves to Secure Your Future

Aug 5, 2025Life Insurance Tax Implications 2025: 17 Key Rules & Smart Strategies to Save More

Aug 5, 2025Life Insurance for Diabetics in 2025: What You Qualify For & How to Get Approved Fast

Jul 30, 2025